Rates of interest are more than simply a financial concept. Interest rates should be something that everyone has a basic grasp of since they impact so many parts of our everyday life. Whether you are attempting to save for retirement, take out a loan, or just comprehend the current global economy, this guide will provide the interest rates you will encounter in the most clear way imaginable. So that you can confidently handle interest rates, this article will go over what they are, how they work, how they effect the economy, and your own finances.

The Basics of Interest Rates

Before we dive into the nitty-gritty details, let's start with the basics. Interest rates, simply put, are the cost of borrowing money or the return on invested capital. They represent the percentage that is added to the principal amount over a specified period. Understanding interest rates is crucial because they affect everything from the cost of your mortgage to the returns on your savings.

Definition and Importance of Interest Rates

Interest rates are charges or rates applied to borrowed or invested funds, representing the cost or reward for using or providing capital. They are an essential tool for monetary policy, influencing economic growth, inflation, and employment rates.

Types of Interest Rates

There are various types of interest rates, including the simple rate, the compound rate, the federal funds rate, prime rate, and APR (Annual Percentage Rate). Each type serves different purposes and is applicable in specific financial contexts.

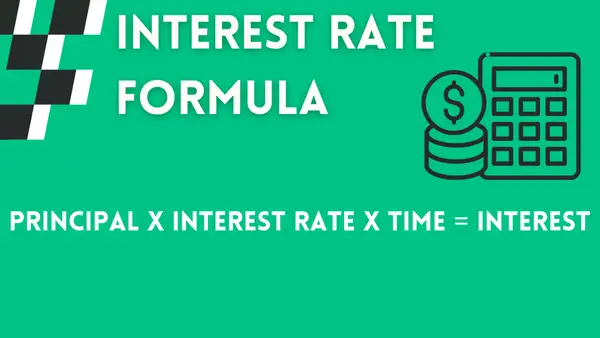

Simple Interest

Calculating simple interest is straightforward. Let's look at the formula you can use to calculate it.

Principal x interest rate x time = interest

Let's illustrate this with an example: Imagine depositing $8,000 into a savings account that offers a 2.5 percent (0.025) interest rate for 4 years. Using the formula, the interest earned over this period would be $8,000 x 0.025 x 4 = $800.

Compound Interest

Compound interest is a bit more complex than simple interest because it involves not only the initial principal amount but also the accumulated interest over time. Here's a simple explanation and example:

Let's say you invest $1,000 in a savings account with a 5% annual interest rate, compounded annually, for 3 years.

Each year, your money grows not just based on the initial $1,000 but also on the interest it earned in previous years. So, each year, you're essentially earning interest on top of interest.

Here's how it works:

- Year 1: You earn 5% interest on $1,000, which is $50. So, your total becomes $1,000 + $50 = $1,050.

- Year 2: Now, you earn 5% interest on $1,050, not just on the original $1,000. That's $52.50 in interest. So, your total becomes $1,050 + $52.50 = $1,102.50.

- Year 3: Again, you earn 5% interest on $1,102.50. That's $55.13. Your total becomes $1,102.50 + $55.13 = $1,157.63.

So, after 3 years, your initial $1,000 has grown to $1,157.63 due to compound interest.

The Mechanics of Interest Rates

Now that we have a solid understanding of the basics, let's explore how interest rates are calculated and what factors influence them.

How Interest Rates are Calculated

The calculation of interest rates depends on several factors, such as the risk associated with the loan, inflation expectations, creditworthiness of borrowers, and the prevailing market conditions. Banks and financial institutions use complex models and algorithms to determine interest rates for loans and other financial products.

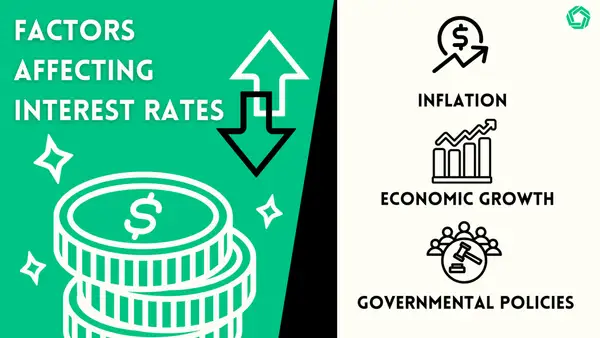

Factors Influencing Interest Rates

Borrowing costs and investment returns, or interest rates, are affected by a number of variables that mirror the state of the economy and governmental policies.

One major element is inflation, which is defined as a general rise in prices across the board. A rise in inflation causes money's buying power to fall over time, prompting lenders to ask for higher interest rates. One way central banks manage economic activity and price stability is by adjusting interest rates in reaction to inflation.

One of the most important factors in interest rate determination is economic growth. The demand for credit tends to rise in tandem with an expanding economy, which is marked by more employment, increased consumer spending, and more investment from businesses. Lenders may try to take advantage of the opportunity given by a flourishing economy, which might lead to higher interest rates due to the increased demand. In contrast, when the economy is in a slump, policymakers may decide to cut interest rates in an effort to revive borrowing and spending.

Interest rates are greatly affected by governmental policies, especially those enacted by fiscal authorities and central banks. Interest rates in the economy are influenced by central banks, who use monetary policy instruments such as benchmark interest rates. Interest rates are indirectly impacted by fiscal policies, which include government spending and taxation. Interest rates can rise due to large government deficits or excessive borrowing because investors are looking for greater returns to offset the risk of lending to governments with high debt levels.

Additionally, lending criteria and interest rate dynamics within financial markets can be influenced by regulatory policies and actions that attempt to ensure financial stability. Credit availability and costs are affected by these policies, which influence the lending and borrowing environment.

Inflationary pressures, government policies, regulatory frameworks, economic circumstances, and overall economic health all interact intricately to determine interest rates. Since interest rates significantly affect borrowing costs, investment returns, and overall economic performance, it is critical for policymakers, investors, and consumers to understand these issues.

Interest Rates and Personal Finance

Interest rates play a pivotal role in shaping the landscape of personal finance, directly influencing the accessibility and affordability of various financial products. Let's delve deeper into how interest rates impact loans and savings and discuss effective strategies for navigating through fluctuations.

How Interest Rates Affect Loans and Savings

Interest rates profoundly affect both borrowing and saving. Higher interest rates translate to increased borrowing costs, elevating expenses associated with mortgages, auto loans, and credit cards. Conversely, higher interest rates also imply higher returns on savings vehicles such as savings accounts, certificates of deposit (CDs), and other investments.

When interest rates rise, the cost of borrowing escalates, making it more expensive for individuals to finance large purchases or carry balances on credit cards. However, savers can benefit from higher yields on their deposits, earning more interest on their savings over time.

Conversely, in a low-interest-rate environment, borrowing becomes more affordable, prompting individuals to consider taking out loans for various purposes. However, savers may find their returns diminished, as interest rates on savings accounts and other conservative investments tend to decrease.

Strategies for Navigating Changing Interest Rates

Given the dynamic nature of interest rates, it's imperative to adopt strategies that can help mitigate their impact on personal finances. During periods of low interest rates, individuals may seize opportunities to refinance existing loans, such as mortgages or student loans, at lower rates. This can result in substantial savings over the loan term.

Additionally, consolidating high-interest debt into a single, lower-rate loan can alleviate financial strain and expedite debt repayment. This strategy can be particularly advantageous when interest rates are expected to rise in the future.

Conversely, when interest rates are on the uptrend, locking in fixed-rate loans can provide stability and protection against future rate hikes. Fixed-rate mortgages, in particular, offer predictability in monthly payments, shielding borrowers from the impact of rising interest rates.

Moreover, as investors navigate the ever-changing landscape of financial markets, it is imperative to maintain a diversified portfolio to protect against fluctuations in interest rates. By maintaining a balance between fixed income securities, equities and alternative investments, individuals can effectively manage risk while striving to achieve optimal returns. Working with an experienced financial advisor is highly recommended to create an investment strategy tailored to one's specific goals and risk tolerance levels.

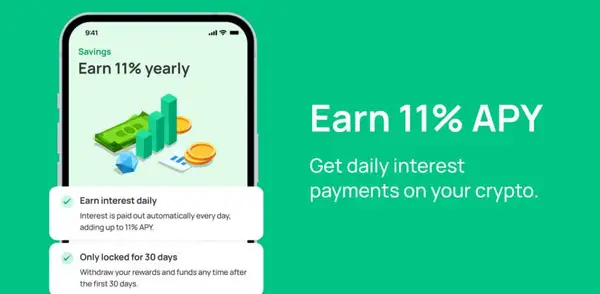

In line with this approach, consider exploring the opportunity to diversify your portfolio through Morpher Savings. Offering a reliable way to earn guaranteed returns on your MPH tokens, Morpher Savings functions like a virtual savings account in the cryptocurrency world. With an attractive 11% Annual Percentage Yield (APY), this platform offers an attractive opportunity to increase your earnings. By staking your MPH tokens, you will start accruing daily interest at 0.03%, laying the groundwork for a steady growth in your savings over time. Don't miss out on claiming your special bonus – join Morpher Savings today and witness your wealth grow.

Impact of Interest Rates on the Economy

Interest rates have a far-reaching impact on the economy, affecting inflation, employment rates, and the overall stability of the financial system.

Interest Rates and Inflation

Interest rates and inflation share a complex relationship. High interest rates can be employed by central banks to curb inflation, as borrowing becomes more expensive, reducing consumer spending and slowing economic growth. Conversely, low interest rates can stimulate borrowing and spending, boosting the economy but potentially leading to higher inflation rates.

Interest Rates and Unemployment

The relationship between interest rates and employment is influenced by various factors. Lower interest rates can encourage businesses to expand, invest, and hire more employees. Conversely, higher interest rates may impede growth and result in reduced job creation. Central banks carefully assess these dynamics when setting interest rates.

Global Perspective on Interest Rates

Interest rates not only impact individual countries but also have profound implications on the global financial landscape. Let's explore how interest rates vary around the world and their relationship with exchange rates.

Comparing Interest Rates Around the World

Interest rates differ from country to country, as they are influenced by unique economic, political, and social factors. Some countries may have higher interest rates to combat inflation, while others may have lower rates to stimulate economic growth.

International Interest Rates and Exchange Rates

The relationship between interest rates and exchange rates is complex. Higher interest rates can attract foreign investment, strengthening the local currency. Conversely, lower interest rates may lead to capital outflows, weakening the currency. Understanding these dynamics is crucial for businesses engaged in international trade and investors with global portfolios.

Integrating Carry Trade Strategy

In the global perspective on interest rates, the carry trade strategy plays a significant role. This strategy involves borrowing in a low-interest-rate currency and investing in a high-interest-rate currency to profit from the interest rate differential.

For instance, if the interest rates in Country A are higher than those in Country B, investors may borrow in Country B's currency (where rates are lower) and invest in Country A's currency (where rates are higher). By doing so, they aim to capture the interest rate differential as profit.

However, carry trades involve risks, including exchange rate fluctuations and changes in interest rate differentials. Sudden shifts in market sentiment or unexpected policy changes can lead to losses for carry trade investors.

FAQs

What are interest rates?

Interest rates are charges or rates applied to borrowed or invested funds, representing the cost or reward for using or providing capital.

How are interest rates calculated?

Interest rates are calculated taking into account factors such as the risk associated with the loan, inflation expectations, creditworthiness of borrowers, and prevailing market conditions.

What factors influence interest rates?

Interest rates are influenced by factors such as central bank policies, inflation, economic growth, government actions, investor sentiment, and global market conditions.

How do interest rates impact the economy?

Interest rates have a significant impact on inflation, employment rates, economic growth, and the stability of the financial system.

How do interest rates affect personal finance?

Interest rates affect personal finance by influencing the cost of loans, the returns on savings, and the overall affordability of financial products.

How can individuals navigate changing interest rates?

To navigate changing interest rates, individuals can consider refinancing loans, consolidating debt, exploring fixed-income investments, and diversifying their portfolios.

What is the global perspective on interest rates?

Interest rates vary around the world due to unique economic, political, and social factors. These rates influence exchange rates and have implications for businesses and investors with global exposure.

By gaining a comprehensive understanding of interest rates, we can make informed decisions about our finances, seize opportunities, and navigate the ever-changing financial landscape. Whether it's analyzing market trends or exploring strategies to mitigate risks, a solid grasp of interest rates can unlock a wealth of possibilities. Stay curious, keep learning, and let your newfound knowledge empower you on your financial journey.

With a deeper understanding of interest rates and their impact on the financial world, it's time to seize control of your investment journey. Enjoy the benefits of zero fees, unlimited liquidity, and the opportunity to trade various asset classes with Morpher. Use your understanding of interest rates to enhance your investment approach. Explore fractional investing, leverage market trends, and secure your assets with Morpher for a distinctive trading experience. Sign up now to receive your free bonus and begin putting your knowledge into practice with Morpher.

Disclaimer: All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, or individual’s trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs. This post does not constitute investment advice.

Painless trading for everyone

Hundreds of markets all in one place - Apple, Bitcoin, Gold, Watches, NFTs, Sneakers and so much more.

Painless trading for everyone

Hundreds of markets all in one place - Apple, Bitcoin, Gold, Watches, NFTs, Sneakers and so much more.