What Is Dollar Cost Averaging? A Complete Guide to Stress Free Investing

by Matthias Hossp

Share:

Investing can feel overwhelming. One day, the market is flying high. The next, it’s crashing. And for anyone trying to pick the “perfect moment” to buy in, it can feel like a never ending game of what if?

Even professionals fall into this trap. In our office, we hear it all the time “I should have bought more Bitcoin,” or “Why didn’t I add more to that position?” It’s enough to make you wonder if we’re all just living in some alternate reality where we made the right decisions.

That’s exactly why we decided to create the ultimate guide to Dollar Cost Averaging (DCA), one of the simplest, yet most effective investing strategies out there.

This strategy takes the guesswork out of investing, giving you a steady, low-stress way to build wealth without obsessing over market timing. It doesn't matter if you're new to investing or just looking for a more disciplined approach, this guide will walk you through everything you need to know:

- What DCA is and why it works

- How to start using DCA (step by step)

- When DCA is the right strategy and when it’s not

- Real-world examples (including S&P 500 gains over time)

- How DCA compares to other investing strategies such as Lump Sum

By the end, you’ll know whether DCA is right for you and more importantly, how to use it effectively.

What Is Dollar Cost Averaging?

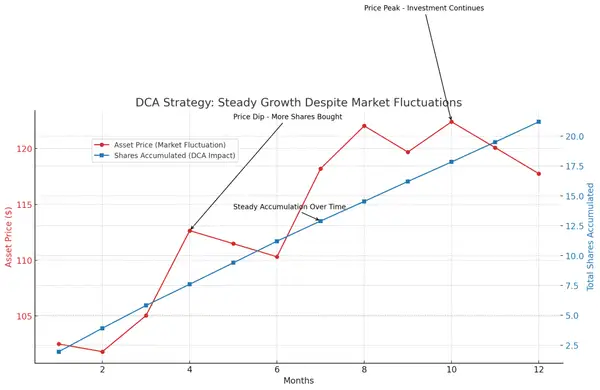

Dollar Cost Averaging (DCA) is an investment strategy where you invest a fixed amount of money into an asset at regular intervals, no matter what the market is doing. Instead of investing everything at once, potentially at a bad time, you spread out your purchases over time. By consistently buying, you average out your purchase price, making it easier to stay invested without worrying about short-term market swings.

The idea? You avoid making emotional decisions and benefit from market fluctuations.

📌 Example:

Imagine you invest $500 per month into Bitcoin. Some months, Bitcoin is trading at $100,000, while other months, it dips to $80,000 or even lower. By consistently buying every month, you average out your purchase price, sometimes buying high, sometimes buying low, but never going all-in at the worst possible moment.

DCA is the opposite of trying to time the crypto market, which, let’s be honest, even the most seasoned traders struggle to do successfully. Instead of stressing over when to buy, you stick to a steady plan and let time do the heavy lifting.

How Does Dollar Cost Averaging Work?

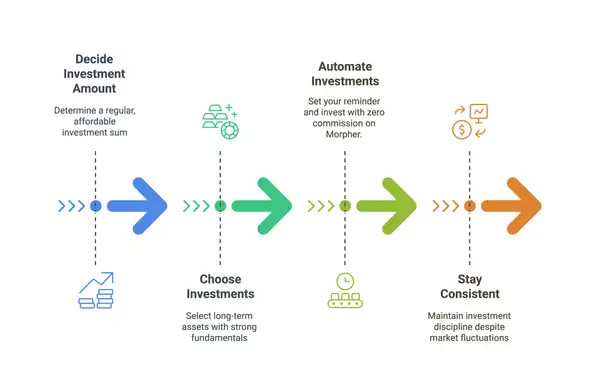

DCA is easy to implement, and pretty much anyone can do it. Here’s how:

Step 1: Decide How Much You Can Invest

Your investment should be an amount you can afford to invest regularly, whether it’s $100 a week, $500 a month, or $5,000 a quarter.

💡 Key Tip: Set aside a fixed percentage of your income like 10% of every paycheck to invest automatically.

Step 2: Choose Your Investments

On Morpher, you can use DCA with a wide range of assets, including stocks, forex, and cryptocurrencies. DCA works best with long-term assets that you believe in, such as:

- Index Funds (like the S&P 500)

- Blue-chip Stocks (Apple, Microsoft, etc.)

- Cryptocurrencies (Bitcoin, Ethereum, etc.)

🚨 Warning: DCA won’t magically turn a bad investment into a good one. Pick assets with strong fundamentals.

Step 3: Automate Your Investments

Some brokers allow automatic purchases, making investing effortless. This removes the temptation to “wait for a better price”, a habit that often leads to missed opportunities.

💡 Key Tip: At Morpher, we believe in giving you full control over your trading decisions, so automated payments aren’t available yet. However, you can easily stick to your DCA plan by setting a recurring reminder and placing your trades manually with just one click.

Here’s how to stay on track:

✔️ Set a recurring reminder: Use your phone or calendar to schedule your investment day (weekly or monthly).

✔️ Fund your Morpher account: Deposit funds using GBP, USD, Euro (via SEPA transfer), or cryptocurrencies.

✔️ Log in to Morpher: Open the platform when your reminder pops up.

✔️ Select your asset: Choose the stock, forex pair, or cryptocurrency you want to invest in.

✔️ Enter your trade: Input the fixed amount you’ve decided to invest (e.g., €200 in Bitcoin).

✔️ Confirm & repeat: Since Morpher has zero commissions, your entire deposit gets invested, no hidden fees eating into your returns.

By following this simple process consistently, you’ll build your portfolio over time without stressing over market timing.

Step 4: Stay Consistent (Even When It Hurts)

The hardest part? Sticking to your plan.

- When markets crash, you’ll feel like stopping. Don’t.

- When stocks skyrocket, you’ll want to go all in. Stay steady.

Over time, DCA works because you’re investing in both the good times and the bad.

When Should You Use Dollar Cost Averaging?

DCA isn’t a one-size-fits-all strategy, but it’s great for:

🚨 When DCA Is Not Ideal:

If you already have a large lump sum sitting in cash, you may be better off investing it immediately instead of waiting to spread it out over time.

Best Markets for DCA

Dollar Cost Averaging is a powerful strategy, but its effectiveness also depends on the type of asset you're investing in. Generally, DCA works best in markets where long-term growth potential outweighs short-term volatility. Here’s a deeper look at the markets where DCA shines:

Stocks: A Long-Term Wealth Builder

DCA is an excellent approach for stock market investing, particularly for blue-chip stocks and index funds. Since equities tend to rise over time, regularly investing helps you build wealth while reducing the risk of making a large purchase at a market peak.

Best for:

- Index Funds (e.g., S&P 500, Nasdaq-100): These track the overall market and have a strong historical trend of growth.

- Large-Cap Stocks (e.g., Apple, Microsoft, Amazon): These companies have strong fundamentals and are less volatile than smaller stocks.

DCA may not be ideal for highly speculative or small-cap stocks. If a company has weak fundamentals, averaging into a losing investment won’t help.

Crypto: Managing Volatility in Digital Assets

Cryptocurrency is notorious for high volatility, making it a strong candidate for DCA. Prices can swing 10-20% in a day, and timing the market is nearly impossible. DCA helps smooth out these fluctuations by spreading purchases over time.

Best for:

- Bitcoin & Ethereum: Established assets with long-term adoption trends.

- Blue-chip altcoins: Assets with real-world utility and strong developer activity.

DCA may not be ideal for Meme coins or speculative tokens. Averaging into assets with no real utility can be risky.

Other Markets: Does DCA Work Everywhere?

Forex & Commodities: DCA is less effective because these markets are often cyclical or influenced by macroeconomic trends. If you’re trading currencies or gold, timing and macroeconomic analysis matter more than long-term averaging.

Real Estate: DCA isn’t commonly used here since buying property requires large lump sums, but it can apply to Real Estate Investment Trusts (REITs), which trade like stocks.

Does DCA Actually Work? (Real Example)

Let’s assume you invested $500 per month into the S&P 500 from March 2019 to March 2024.

- Total invested: $30,000 (500 x 60 months)

- S&P 500 performance over this period: Roughly ~11-12% annual return

- Final portfolio value (as of early 2024): ~$47,500

- Total gain: ~58% return

Even with market ups and downs including crashes like the COVID-19 drop in 2020, a consistent investment strategy delivered strong long-term growth.

What If You Had Waited to “Time the Market”?

A common argument against DCA is “Why not wait for a dip?” But timing the market is extremely difficult even professionals struggle with it.

Data shows that missing just a few of the best market days can drastically hurt returns:

- If you stayed fully invested from 2003-2023, the S&P 500 returned 9.8% per year.

- Miss the 10 best days? Your annual return drops to 5.6%.

- Miss the 20 best days? You get just 3.2% per year.

- Miss the 30 best days? Your return shrinks to a mere 1.8%—barely above inflation.

Investors who wait for the “perfect” entry point often miss major rallies and underperform those who simply invest consistently through DCA.

What If the Market Is High? Should You Still Use DCA?

Right now, the stock market is near all-time highs. Should you still use DCA?

Yes, because historically, all-time highs don’t mean necessarily future crashes.

For example, if you had started DCA in 2007 before the Great Recession, your investments would have dropped short-term… but over time, they would have recovered and grown significantly.

To sum it up all together, trying to “wait for a better time” often leads to never investing at all.

DCA vs. Lump-Sum Investing: Which Is Better?

| Factor | Dollar Cost Averaging (DCA) | Lump-Sum Investing (LSI) |

|---|---|---|

| Strategy | Invest a fixed amount at regular intervals (e.g., monthly) | Invest the entire amount at once |

| Best for | Managing risk, avoiding emotional investing, smoothing out volatility | Maximizing long-term returns by being fully invested earlier |

| Market Timing Risk | Lower risk—gradual investing reduces the impact of buying at a peak | Higher risk—investing everything at once could lead to short-term losses if the market drops |

| Historical Performance | Generally underperforms lump-sum investing over long periods | Outperforms DCA ~75% of the time over long-term horizons |

| Volatility Impact | Helps manage market ups and downs by buying at different prices | Full exposure to market volatility immediately |

| Psychological Comfort | Easier to stick with—removes pressure from market timing decisions | Can be stressful if the market drops right after investing |

| Ideal Market Conditions | Works well in volatile or uncertain markets | Works best in consistently rising markets |

| Example (S&P 500, 5 years, $30,000 investment) | Investing $500 per month from 2019-2024 would have grown to ~$47,500 | Investing $30,000 at once in 2019 would have grown to ~$63,000 |

| Downside Risks | If markets rise consistently, you may miss out on gains by waiting to invest | Higher short-term risk—could enter at a bad time (e.g., before a crash) |

| Who Should Use It? | Investors who want less stress, steady investing, and risk management | Investors who want higher returns and can tolerate short-term losses |

Final Thoughts: Should You Use Dollar Cost Averaging?

Dollar Cost Averaging is one of the most accessible and reliable investment strategies for long-term investors. It removes the stress of market timing, encourages consistency, and helps navigate volatility without the fear of buying at the wrong time.

That being said, DCA isn’t for everyone. It works best for those who prefer steady investing and risk management, while lump-sum investing may be the better choice for those who can tolerate short-term fluctuations and want to maximize long-term returns.

DCA is a strong choice if:

- You want to invest steadily without worrying about market timing

- You have a long-term mindset and prioritize consistency over quick gains

- You prefer to reduce risk and avoid emotional investing

DCA may not be ideal if:

- You have a lump sum ready to invest and are comfortable with volatility

- You want to actively trade and time the market instead of following a passive approach

The Bottom Line

If you’re looking for a simple, disciplined, and stress-free way to invest, DCA is an excellent place to start. It keeps you in the market, smooths out volatility, and historically delivers solid long-term returns.

Ready to start building wealth—without the stress?

👉 Create your Morpher account and start investing today.

Disclaimer: All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, or individual’s trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs. This post does not constitute investment advice.

Painless trading for everyone

Hundreds of markets all in one place - Apple, Bitcoin, Gold, Watches, NFTs, Sneakers and so much more.

Painless trading for everyone

Hundreds of markets all in one place - Apple, Bitcoin, Gold, Watches, NFTs, Sneakers and so much more.